On April 26, 2023, the International Auditing and Assurance Standards Board (IAASB) issued for public comment an Exposure Draft, proposed International Standard on Auditing (ISA) 570 (Revised 202X), Going Concern. Comments were due August 24, 2023.

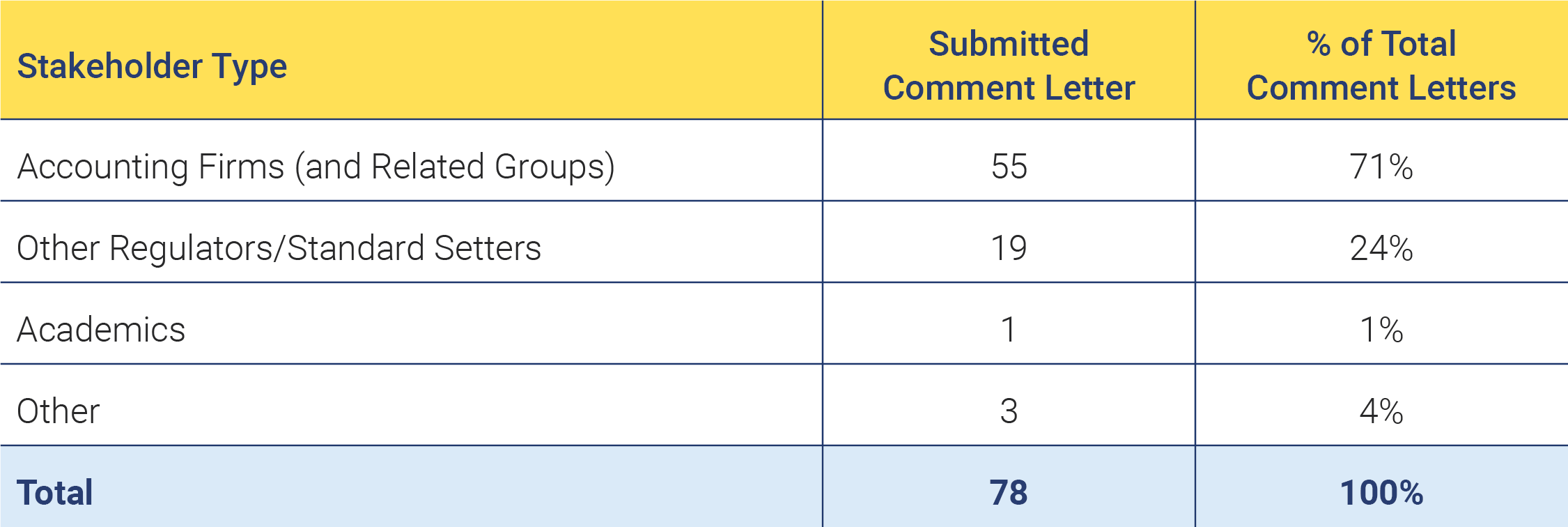

The IAASB received 78 letters, primarily from accounting firms and accounting organizations.

Who responded?

In our analysis of comment letters received, key themes are:

- There is a need for enhanced coordination with the International Accounting Standards Board (IASB).

- There is support for enhanced focus on risk assessment and mixed views on scalability.

- There is support to explore enhanced transparency but mixed views on proposed “Going Concern” section in the auditor’s report.

Three takeaways we had from the feedback the IAASB received in response to their proposal:

- Increased transparency to financial statement users about going concern considerations cannot be solved with an auditing standard alone.

- Linking the design and performance of audit procedures to the auditor’s risk assessment will enable the auditor to use professional judgment when determining and executing their audit response.

- Facilitating a robust dialogue between auditors and investors to understand what investors are expecting and how changes to the auditing standards could enable auditors to meet those expectations could help the IAASB and PCAOB in finalizing their proposal. The IAASB received no comment letters from investor or investor organizations. However, an academic submitted a comment letter based on research they conducted to understand how investors respond to the changes to the auditor’s report proposed in ED-570. The research found that management commentary related to going concern makes a difference for investors. The researchers also found that investors may struggle to distinguish between going concern disclosures about serious issues (like a material uncertainty) versus less serious issues (events or conditions were identified but no material uncertainty exists).

The CAQ will continue to monitor the IAASB’s project on Going Concern. The IAASB is currently considering the comments received on ED-570 and according to their project timeline are targeting final approval of the revisions in December 2024.

For more details, read our full analysis here.